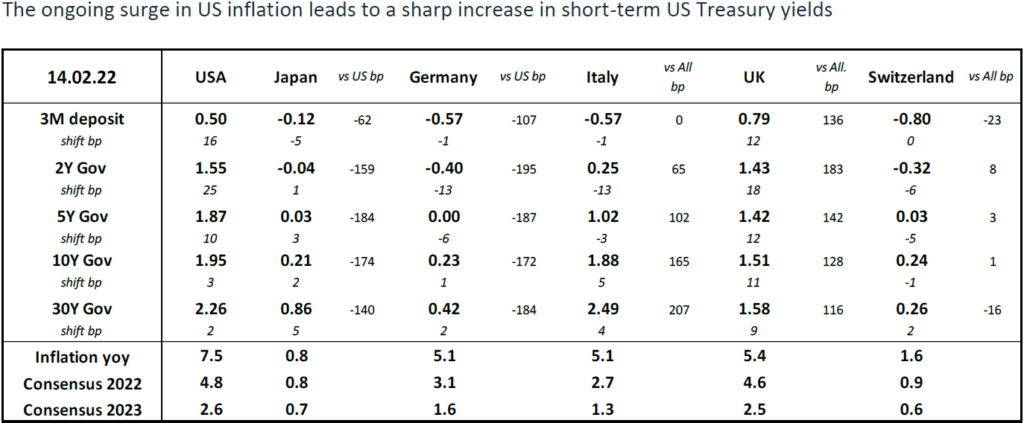

Macro

Macro After three misses, the Fed has a problem

Evidence of persistent inflationary pressures in the US is pushing government bond yields higher.

Corporate

Corporate  Macro

Macro The monetary hawk, an endangered species

Increasing central bank dovishness pushed US and European government bond yields lower.

Macro

Macro “Higher for longer”, the sequel

Recent events are likely to confirm the FOMC's wait-and-see stance, which is not without its dangers.

Macro

Macro Will two doves make a summer?

Friendly comments by Jerome Powell and Christine Lagarde foreshadow first interest rate cuts in June.

Macro

Macro Wall Street peaks, but the economy falters

Recent, but not yet conclusive, indicators point to a deterioration in the US economy.

Macro

Macro The Fed and the ECB are in no hurry

The US central bank's patience is fully justified, but the ECB's wait-and-see attitude is questionable.

Macro Renewed realism and healthy correction

Investors have reassessed the prospects for interest rate cuts amid sticky US “core” inflation.

Corporate

Corporate H2 and Full-Year 2023 Financial Results

2023 was another successful year for ONE swiss bank SA, brimming with achievements and culminating in healthy financial results.

Macro

Macro The Fed’s pivot? Not before May 1st

Powell's comments and the strength of the US economy invite investors to be patient.